Time to read: 5 minutes |

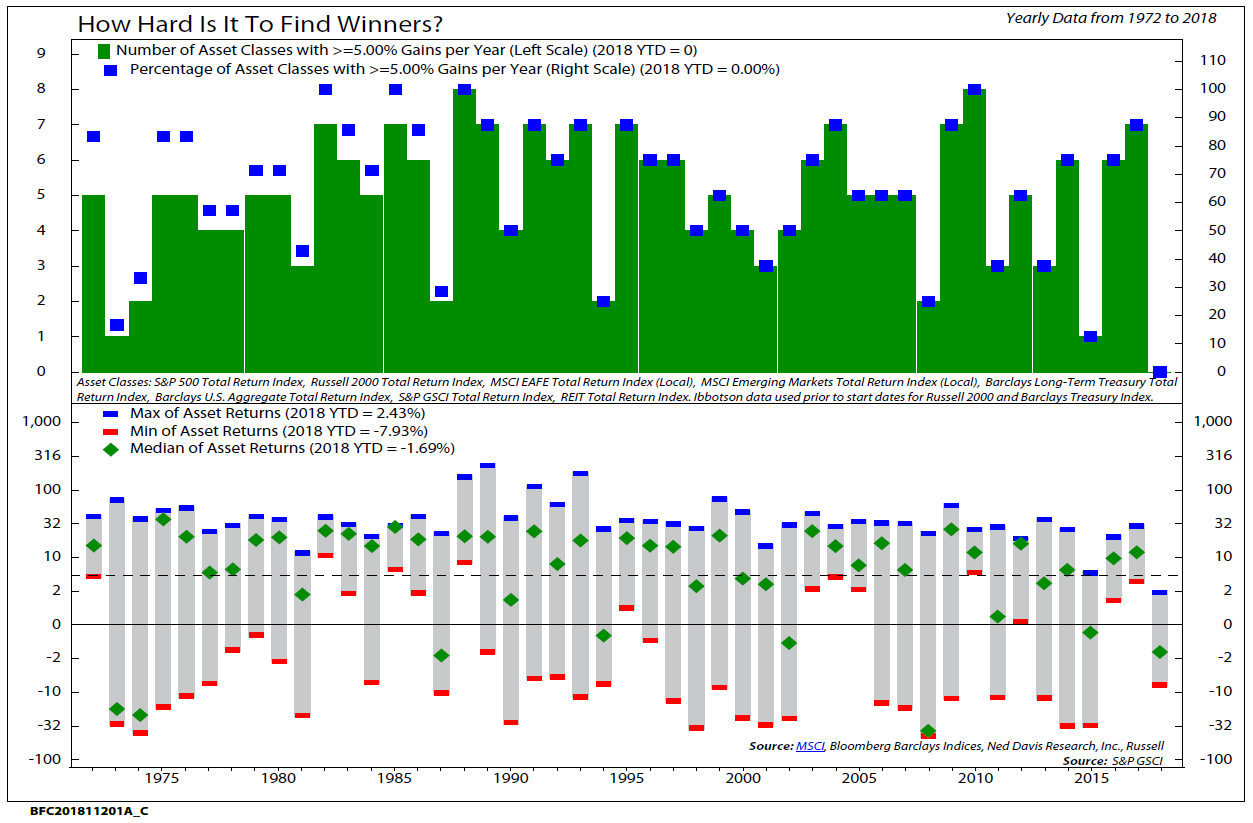

It appears 2018 will be the first year since 1972 when no major asset class returned 5% or more. Global quantitative tightening could be the culprit according to Ed Clissold, Chief U.S. Strategist at Ned Davis Research.

While the Federal Reserve has been trimming its balance sheet for over a year, Ned Davis Research estimates that November 2018 is the first month in which combined central bank policies around the world are resulting in global quantitative tightening (higher interest rates and smaller balances on central bank balance sheets).

Quantitative easing during and after the Great Recession produced massive asset price inflation. Over the past nine years, these large gains have come with concerns about how asset prices will behave when the ultra-easy monetary policy inevitably comes to an end. Global asset prices may already be feeling the pinch.

The chart below shows annual returns for eight major categories of asset classes: U.S. large-caps, U.S. small-caps, international developed, emerging markets, U.S. Treasuries, U.S. aggregate bonds, commodities, and real estate. This year is the first since 1972 in which no asset class has returned at least 5%.

The median return for these asset classes since January 1, 2018, is -1.7%. Median returns even during times of severe recessions, such as 2008 (-37%) and 1974 (-22%), still included at least one asset class that rallied (Treasury bonds in 2008 and commodities in 1974.) In other words, historically there has always been a bull market somewhere.

The goal of central bankers is to lend support to asset prices in times of need, but then pass the baton to the real economy. While this goal was achieved over the past nine years, it appears monetary policy may increasingly become a headwind for major assets, rather than the tailwind it has been in recent history.

Stratos Private Wealth portfolios maintain their underweight allocation to stocks, and overweight allocation to bonds (with shorter duration/interest rate sensitivity.) This allocation is consistent with increased bear market risk, as indicated by Ned Davis Research’s tactical indicators. However, the secular bull market remains intact, making it highly unlikely we’re headed for a bear market of 2007-2009 proportions.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful. All indices are unmanaged index which cannot be invested into directly. Past performance is no guarantee of future results.

Stratos Private Wealth is a division through which Stratos Wealth Partners, Ltd. markets wealth management services. Investment advisory services offered through Stratos Wealth Partners, Ltd., a registered investment adviser. Stratos Wealth Partners and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only; and is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. You should consult your own tax, legal, and accounting advisors before engaging in any transaction. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. To determine which strategies or investments may be suitable for you, consult the appropriate qualified professional prior to making a decision. Investing involves risk including possible loss of principal. Some of the information contained herein has been obtained from third party sources which are reasonably believed to be reliable, but we cannot guarantee its accuracy or completeness. The information should not be regarded as a complete analysis of the subjects discussed.

{kind=link}