Time to read: 7 minutes |

- Economic growth drives profits, which should help fuel long-term gains in stocks through 2019.

- Most economic sub-cycles are still young, there’s little debt creation and consumer confidence is high.

- There’s no over investment, tighter conditions or shocks— which often precede recession.

How much further can the U.S. expansion go? Although no one really knows, it could extend beyond the consensus of 2020. One of the most enduring features of this recovery is the absence of economic imbalances. Furthermore, the long-term bull market in stocks, which started in March 2009, should be supported by a continuing U.S. expansion.

Here are three reasons why the U.S. expansion has more room to run:

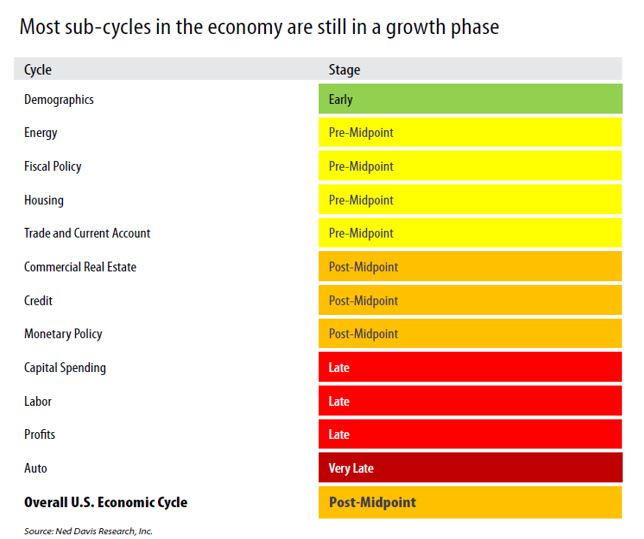

1. Most economic sub-cycles are only near their midpoints.

The U.S. economic cycle is comprised of many sub-cycles in specific areas (such as credit and housing), which move from growth to contraction to complete a cycle. Looking at these sub-cycles can show where we are in the overall economic cycle.

Ned Davis Research analyzed a dozen sub-cycles. As shown in the table below, most sub-cycles are still relatively young. Exceptions exist; autos, capital spending, profits and labor all are late-cycle. In sum, however, the sub-cycles suggest the overall U.S. economic cycle is, age-wise, merely beyond its midpoint.

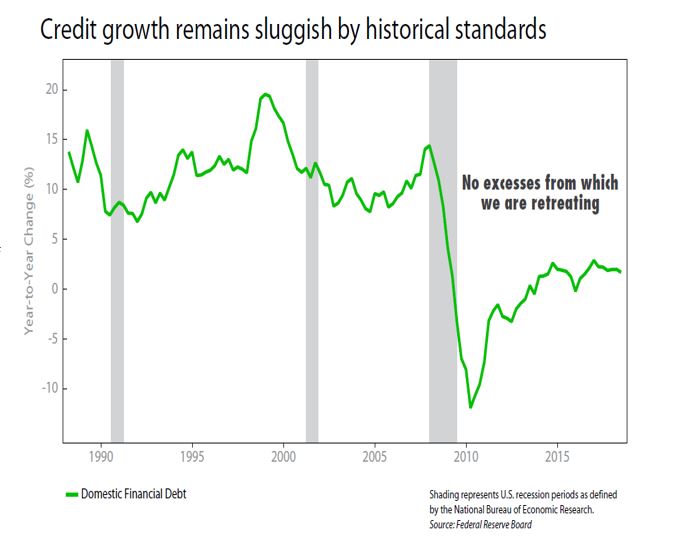

2. Debt creation is lacking.

The growth in debt remains sluggish by historical standards. As shown in the chart below, financial debt is growing less than 3% annually, which is well below the double-digit rates we have seen during past expansions. This lack of debt creation also reduces the risk of a recession since there are no excesses from which we are retreating.

The Federal Reserve Board has raised interest rates eight times since the end of 2015 to increase the cost of borrowing and slow the rate of debt taken on by businesses and consumers. Over time, this has slowed the rate of debt creation by businesses from 9% in 2015 to a current level of only 4.6%.

That said, some economists are concerned with the high level of debt. They argue that while new debt creation has slowed, total credit market debt of $70.7 trillion is high relative to GDP at nearly 350%, and that could drive investor concern as interest rates rise. However, debt relative to net worth has been falling for households and has been relatively stable for businesses. That’s a signal of a lack of excesses that would typically lead to recession.

3. Consumer confidence is high.

Consumer confidence, which is driven by jobs, income, stock prices and housing prices, remains high. This is another buffer against recession, of course, as the American consumer drives more than two-thirds of the economy.

The 2017 Tax Act has been influential in improving consumer confidence. Lower individual income tax rates led to American consumers having more disposable income, which boosted their spending in 2018.

In fact, in the third quarter, consumer spending grew at a 3.6% annual rate. While that’s in line with the average rate during all expansions, consumer spending over the past two quarters was the strongest it has been in the United States since early 2015.

A significant decline in consumer confidence would need to occur before one could conclude that consumer sentiment could result in recession. The Consumer Confidence Index, a measure of how consumers feel about current conditions and the future, typically drops sharply before recessions. Confidence remains high and is far from collapsing.

Why are some analysts bearish?

The basic bearish narrative is that tighter government policies will knock out the economy. Add trade frictions and the advanced age of the current expansion and there seems to be a compelling argument that a recession will happen soon. That outlook seems too simplistic.

Naturally, it is wise to expect slower economic growth going forward. By 2020, the fading impact of the economic stimulus from ultra-low interest rates and tax reform could cause U.S. real GDP growth to slow to around 2% (down from about 3% at the current time, in late December 2018). But that’s a far cry from recession. During the Great Recession of 2007 to 2009, for example, GDP plummeted by -5.1% from peak to trough. By December 2008, GDP had collapsed to a -8.9% annual rate. Stocks followed suit, declining by nearly 54% from October 2007 to March 2009, the worst loss since the Great Depression.

Finally, remember that economic expansions don’t die of old age. They’re killed by over-investment, tighter financial conditions, and shocks. None of these factors currently exist. A U.S. recession doesn’t appear to be around the corner.