Time to Read: 7 Minutes

Many high earners want to know which strategies they can implement to reduce their taxes. In Part I of a 7-part series, “Tax Saving Strategies for High Earners,” we explore the basics and benefits of a tax-reduction strategy called “stacking.” This involves grouping itemized deductions for charitable giving, state/local taxes, and unreimbursed medical costs into single tax years to surpass the standard deduction and receive greater tax deductions over the long term.

What is the difference between the standard deduction and itemized deductions?

When you file your tax return, you have the option of reducing your taxable income in one of two ways. The first option, called the standard deduction, is a flat dollar amount that varies based on your filing status. In 2017, the Tax Cuts and Jobs Act (TCJA) nearly doubled the standard deduction from $6,500 to $12,000 for single filers and $13,000 to $24,000 for married taxpayers filing jointly. The deduction is even higher for taxpayers who are over age 65.

The second option is to use a method called itemizing deductions. If you elect to itemize on your tax return, your taxable income will be reduced by the sum of certain individual tax deductions allowed by the IRS, which could exceed the standard deduction.

How might the higher standard deduction affect my tax benefits?

Given the TCJA’s increased standard deduction and stricter limitations on itemized deductions, fewer taxpayers are benefiting from itemizing because the sum of their itemized deductions no longer exceeds the standard deduction. But some households with itemized deductions just under the standard deduction threshold can still increase their overall tax benefits by itemizing in alternate years through tax-reduction stacking.

How can I stack tax deductions?

The most feasible way to itemize on an alternating basis is by combining large, supplementary or irregular itemized deductions on top of the smaller, recurring, itemized deductions. For instance, you may choose to make a large charitable donation in a year in which you also paid a big medical bill. Stacking these two payments on top of your recurring expenses for mortgage interest, property taxes, and state taxes paid may push the sum of your itemized deductions over the standard deduction threshold. To facilitate a large charitable donation, you may wish to consider opening a Donor Advised Fund (DAF), which allows for a large upfront charitable deduction while maintaining the flexibility to distribute the assets to charities over time.

Who should consider tax-deduction stacking?

If your household has itemized deductions just shy of the standard deduction threshold, you may want to evaluate the potential increased tax benefits available by stacking deductions. Even if your itemized deductions are much greater than the flat standard deduction, stacking can still be beneficial if you need a larger tax break to offset substantial capital gains or earned income in a specific year.

The following hypothetical scenario is meant to describe households who may benefit from stacking now or in upcoming years:

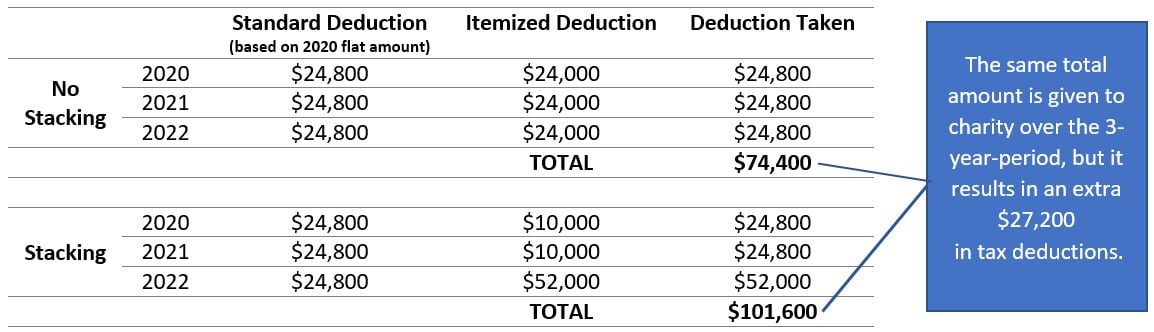

The Jones family aspires to give $14,000 to charity each year. Their itemized deductions will only be $24,000 ($14K for charity + $10K for state and local taxes), which is just shy of the new $24,800 standard deduction in 2020. Thus, they will receive no tax benefit for their charitable contributions or state taxes paid.

If the Joneses were to stack their charitable donations into every third year, their projected itemized deductions would jump to $52,000 ([$14K in charitable donations x 3 years] + $10K for state and local taxes). By stacking charitable donations, their combined deductions over 3 years will equal $101,600 (a $24,800 standard deduction in years 1 and 2, plus $52K in itemized deductions in year 3).

If the Jones family decides not to stack charitable donations, their itemized deductions will never exceed the standard deduction. They will take the standard deduction each year, and their total tax deductions for 3 years will equal $74,400 (the $24,800 standard deduction x 3 years).

By stacking charitable contributions, the Jones family will receive additional tax deductions of $27,200 [S100,800 – $73,200] over 3 years, while still being able to distribute $14,000 annually to their church through a DAF.

On top of that, imagine that Ray Jones has been delaying a medical procedure that will cost him $20,000 out of pocket. The IRS allows an itemized deduction for medical expenses that exceeds 7.5% of Adjusted Gross Income (AGI). Given that the couple’s income dropped from $250,000 to $140,000 in 2020, they may take a tax deduction equal to $9,500 ($20K in medical expense – [7.5% x $140K AGI]). Ray decides to pay the medical bill in a year in which the family stacks their charitable contributions. This will bump the total itemized deductions to $61,500 ($9,500 medical expenses + $53K in other itemized deductions). If Ray had this procedure while the annual household income was $250,000, deductible medical expenses would only equal $1,250 ($20K in medical expense – [7.5% x $250K AGI]). Waiting to incur a large medical expense in a year in which taxable income was lower allowed the Jones family to receive an additional $8,250 ($9,500-$1,250) tax deduction.

Next steps?

To provide an enhanced level of service to our clients, Stratos Private Wealth utilizes a tax-focused financial planning tool, which uncovers potential tax-planning opportunities by analyzing prior years’ tax returns. While we are not tax advisors, our goal is to help clients identify actionable tax-saving strategies worth discussing with their CPAs.

If you need help uncovering potential tax-saving opportunities, please contact us, and we will provide high-level advice that can be evaluated with your CPA. We can then work directly with him or her to put these strategies, like stacking, into action.

.png?width=290&name=Favicon%20SPW%20(1).png)